For most tax offices in the United States, bank products are not optional — they are the difference between closing a return and watching the client walk down the street to the office next door. Refund transfers and refund advances let your clients walk in with nothing in their pocket and walk out with their fee paid and their money on its way. This article explains how each one actually works, why your clients are asking about them, and how to choose a banking partner that will not embarrass you mid-season.

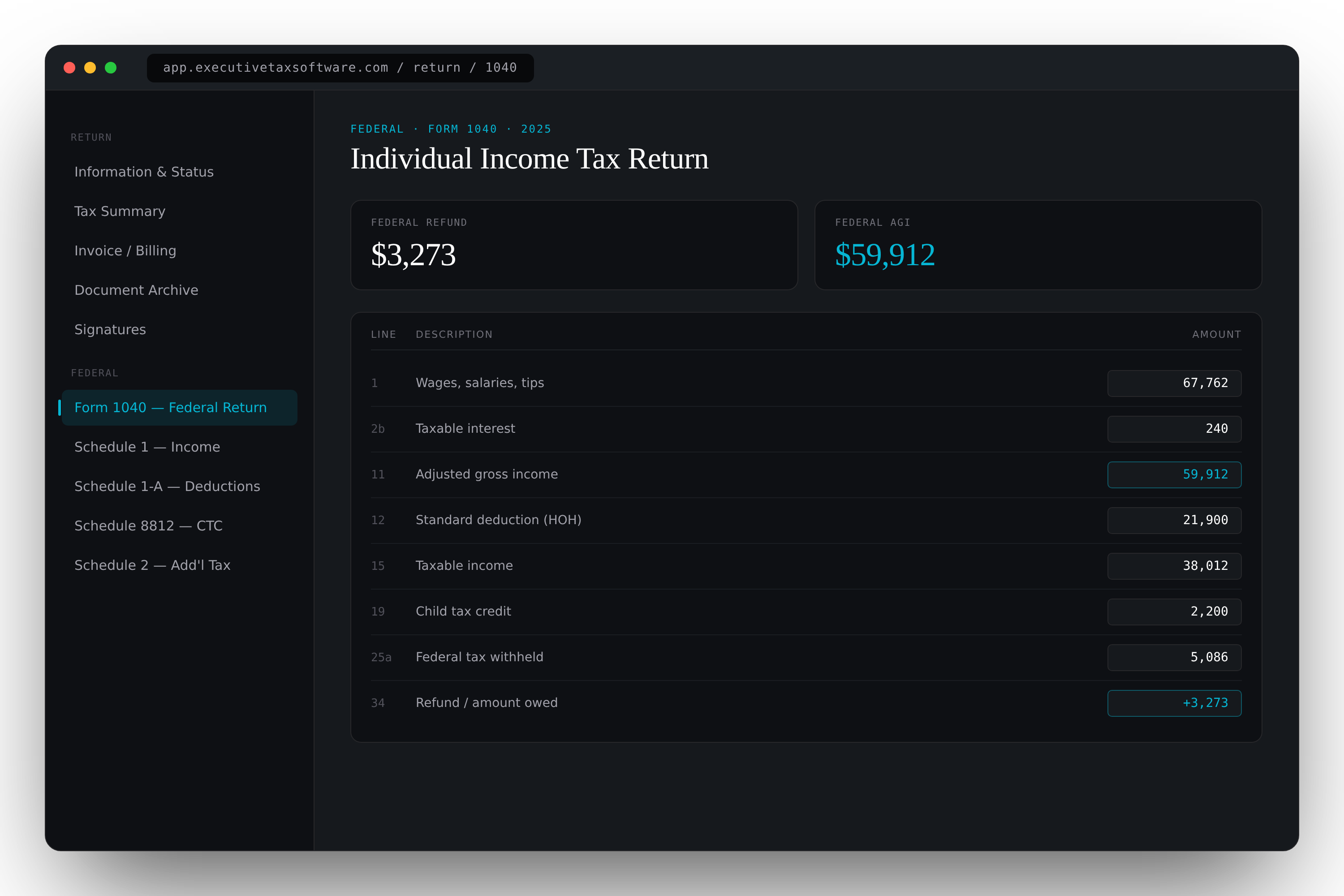

A bank product is a short-term financial product, offered through an IRS-authorized bank, that allows a client to either receive their refund without paying upfront preparation fees or receive a portion of their refund early as a loan. Your tax software integrates with the bank, the IRS sends the refund to the bank, the bank takes its fee and your preparation fee, and the rest is disbursed to the client.

These two terms get used interchangeably, but they are different products with different mechanics, different fees, and different client conversations.

Bank products solve real problems for the people walking into your office. If you are not offering them, the office down the road is — and your client is asking why.

Your tax software determines which banks you can offer. Once you know that list, evaluate each option on the same criteria: advance amounts and approval rates, bank fees, disbursement options (direct deposit, prepaid card, check), settlement speed, and the quality of mid-season support. The cheapest bank fee is meaningless if the bank's approval rate is half what the competing bank approves.

Bank products are subject to specific IRS and bank disclosure requirements. Two non-negotiables every preparer must remember:

“Bank products are where new preparers either build their reputation or lose it. Offer them, explain them honestly, and your clients come back every year. Try to hide the fees and you will not see them again.” — ETS Banking Partners Team

Executive Tax Software ships with direct integrations to multiple IRS-authorized banking partners, so you can compare advance amounts, fees, and approval rates side by side before you sign up — and switch between them year over year if a better offer appears. Our team also handles the enrollment paperwork with the banks on your behalf, which is the single most underrated time-saver of the onboarding process.

Bank products are a multiplier on every other part of your tax office: more clients close, more clients come back, and unbanked clients can finally be served. The right banking partner makes that multiplier reliable. Pick a software that gives you choice between banks, train your staff to explain the products honestly, and you will see the difference in your retention numbers within one season.